Introduction

Recent trends in venture capital reveal a stark transformation in exit strategies. The dramatic reduction of US venture IPOs, coupled with the decrease in M&A activity, underscores a growing reliance on alternative routes for liquidity, such as the secondary market. These markets are emerging as crucial alternatives for firms navigating liquidity challenges and changing investor expectations.

Exits in Turmoil

The venture capital exit landscape has been radically transformed, with a steep decline in traditional exit methods. The cumulative value of US venture IPOs, which constituted 85% of overall VC exit value in 2021, plummeted by 95.9% through September 30, 2023. On a broader scale, VC-backed IPOs hit a decade-long low worldwide.

VC-backed companies that braved the markets did not fare as well as hoped. Take, for instance, Instacart, a Prime Unicorn Index component. Instacart last raised at a $33 billion post-money valuation in 2021 at $125 per preferred share. The company went public at $30 per share in September 2023.

Recent developments have seen high-profile IPOs from companies such as Astera Labs and Reddit, with Rubrik on the verge of its own public offering. While these companies have fared well, startups and investors are still exercising a healthy amount of caution in an IPO market that has yet to fully recover.

M&A exits for VC-backed companies also fell notably, impacted by a challenging regulatory backdrop. High-profile deals, such as Figma’s acquisition by Adobe and iRobot’s by Amazon, collapsed under regulatory pressures.

These developments have extended exit horizons for investors, leaving firms in dire need of liquidity to pay back Limited Partners (LPs). Without cash returned, these LPs are less willing to invest in new funds.

Valuations and Downward Trends

The valuation landscape in the venture capital arena is witnessing a reset. Many companies have delayed fundraising rounds to avoid raising at lower valuations but are beginning to run out of runway. The number of companies raising down rounds has more than doubled in 2023, including previous Index component Truepill, which saw its share price slashed by 93.7% following a cram-down round.

This has led to a slowdown in fundraising for VC-backed companies, with the median time between deals reaching 1.72 years for late-stage companies. This is further evident in overall US dealmaking, which reached a decade low. Mega-rounds, or those worth $100 million or more, were down to 78 deals in Q4 2023 from 429 two years prior. This shift indicates a cautious approach among investors and a recalibration of company valuations.

Fundraising Dynamics

Contrasting with the decline in traditional VC fundraising, secondary funds are experiencing remarkable growth. VC fundraising was down 60.6%, compared to the 180.4% growth experienced by secondary funds. Industry Ventures, Lexington, PineGrove, and StepStone have all reported raising multi-billion dollar secondary funds in the past year, indicating a robust market demand.

This shift is further underscored by the decline in distributions to LPs by US-based VCs, which leaves LPs hesitant to participate in future funds. Distributions fell to $21 billion in 2023, one-seventh of 2021’s levels, highlighting the mounting pressure for liquidity to maintain investor appetite.

Secondary Market Activity

Notable firms in the venture space are increasingly exploring secondary transactions. Tiger, Social, and Insight are considering or have undertaken the sale of startup shares or interest in other funds. Lightspeed is reportedly considering a $1 billion continuation fund in an effort to return capital to its LPs.

Many late-stage companies are using tender offers in place of traditional exit events to provide liquidity to their employees and early investors. Noteworthy companies using or considering this strategy include SpaceX, Databricks, Canva, OpenAI, and Databricks.

Caplight data shows the secondary market gaining momentum towards the end of 2023. Average monthly transactions are up 64.7% from H1 2023 to H2 2023, and there is a 45% growth in the number of companies that were traded more than once over the same period. This trend is evident in the Prime Unicorn Index, which saw a record 15 companies actively traded on the secondary market in Q4, up from 10 in Q3.

Impact on the Prime Unicorn Index

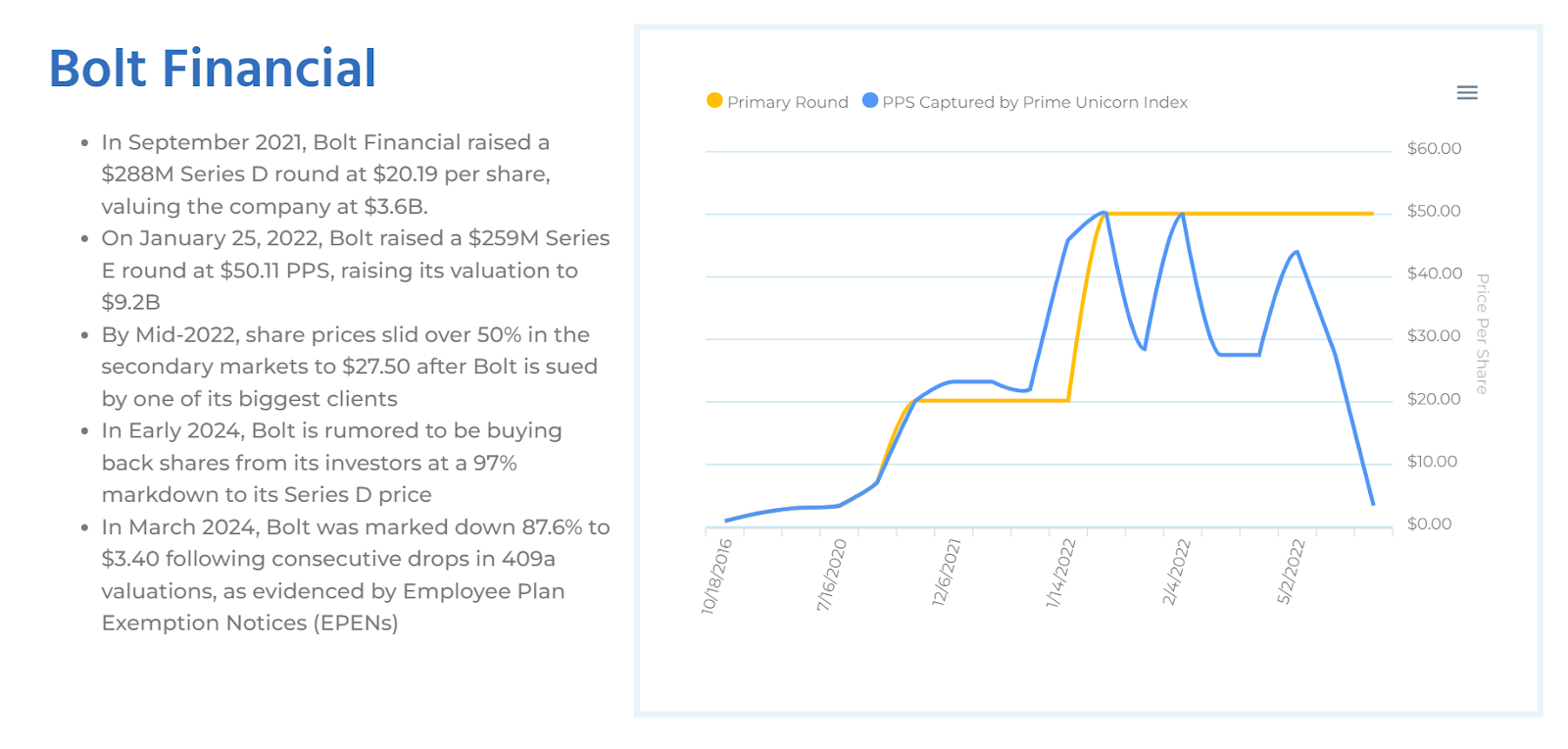

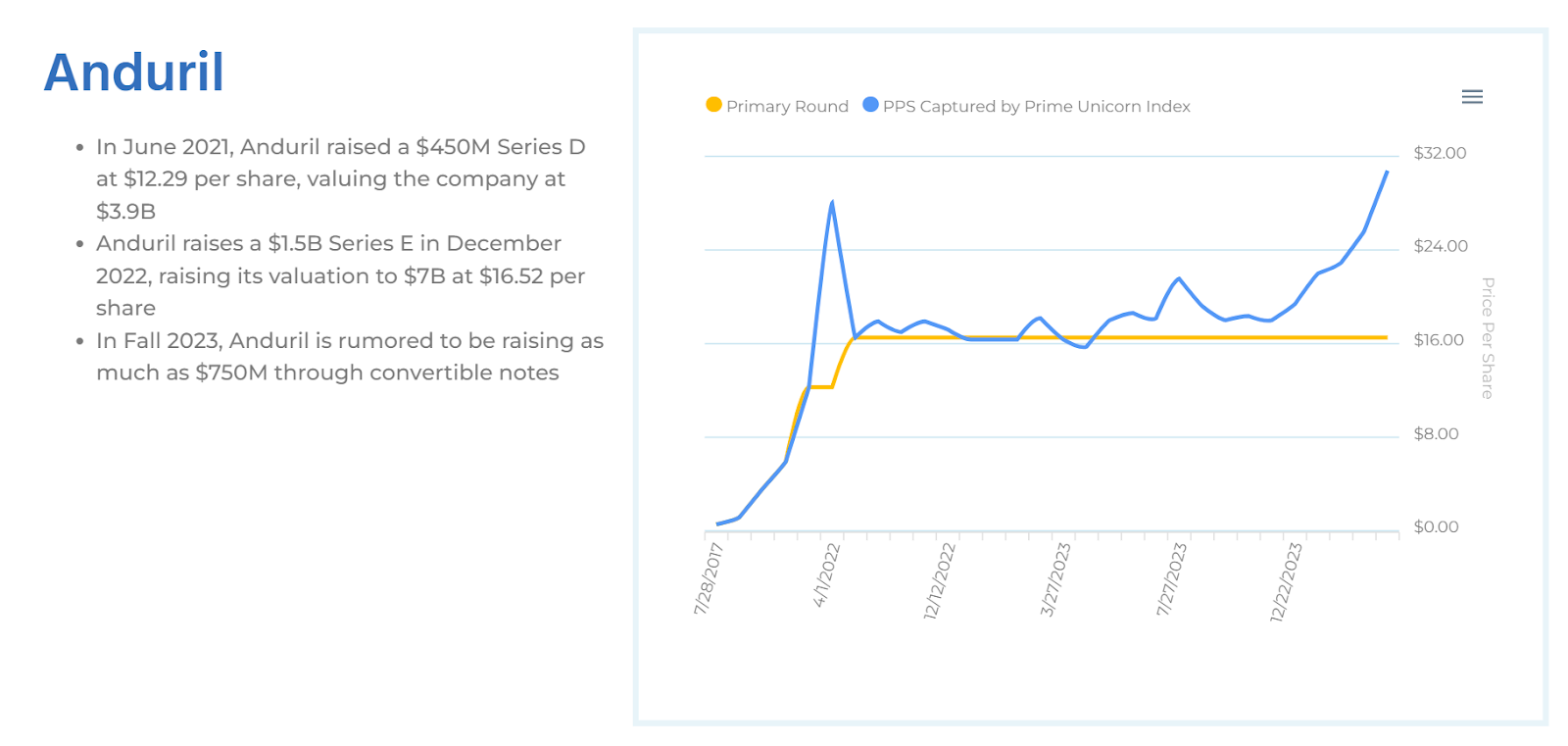

The secondary market offers more immediate and accurate valuations, especially as companies delay new capital raises. The Prime Unicorn Index has seen massive adjustments in company marks using Caplight’s secondary market data. Some of the Index’s largest components, including Brex, Plaid, Bolt, and GoPuff, have witnessed substantial markdowns, while others, such as Anduril and SpaceX, have seen their valuations increase. This variance underscores the dynamic nature of the secondary market valuations.

Conclusion

The rise of secondary markets in venture capital reflects a fundamental shift in the industry’s approach to liquidity and portfolio management. Amidst changing market conditions and evolving investor priorities, secondaries have emerged as a critical mechanism for navigating the venture capital ecosystem. As the industry continues to adapt, the role and influence of secondary markets are poised to expand, potentially reshaping how venture approaches liquidity and valuations.