Vacasa at a Glance

As summer travel hits full swing and families book beach houses, lake cabins, and mountain retreats, it’s the perfect moment to look back at Vacasa, the company that tried to bring big-tech scale to vacation home management. Vacasa was born around a dining room table in 2009, when founder Eric Breon struggled to find a property manager for his family’s vacation home on the Washington coast. With co-founder Cliff Johnson, an attorney he met on Craigslist, Breon built a platform pairing centralized technology with local, on-the-ground service teams, fixing an industry historically fragmented among small local operators. Bootstrapped for six years, Vacasa grew into North America’s largest vacation rental management platform.

The Unicorn Moment

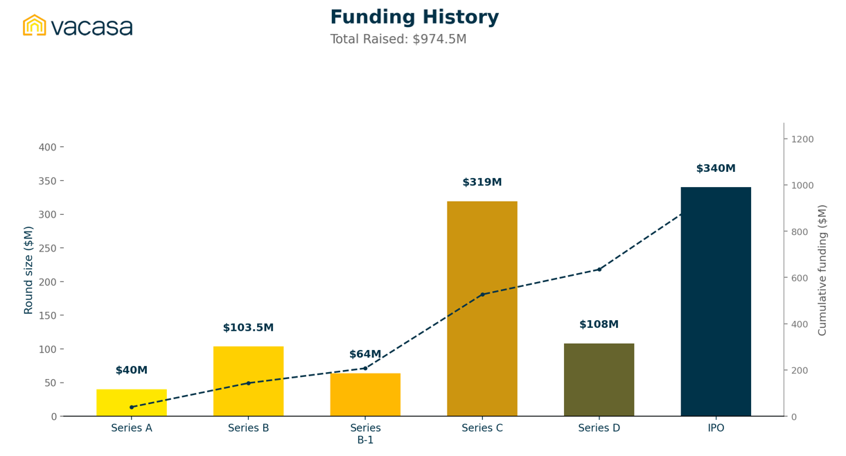

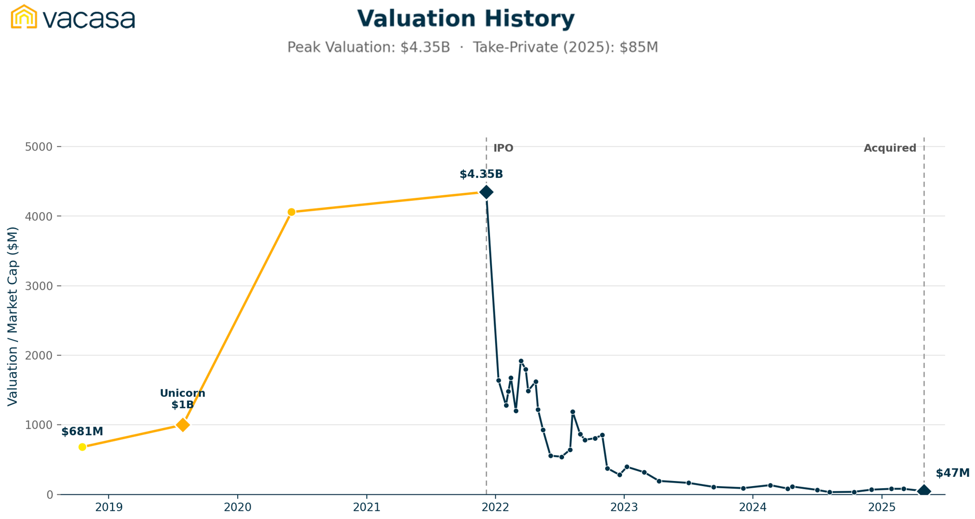

Vacasa crossed into unicorn territory on October 29, 2019, closing a $319 million Series C round led by Silver Lake, with Riverwood Capital, Level Equity, and NewSpring also participating. The round, the largest ever raised in the vacation rental sector, pushed Vacasa’s valuation to “north of $1 billion,” making it the space’s first unicorn. The raise came alongside Vacasa’s $162 million acquisition of Wyndham Vacation Rentals, nearly doubling its portfolio to more than 23,000 managed homes. By then, Vacasa had raised roughly $526.5 million since founding, a rapid ascent for a company that ran six years without outside capital.

Where Vacasa Stands Now

Vacasa went public on December 7, 2021, via a SPAC merger with TPG Pace Solutions, debuting on the Nasdaq as “VCSA” at a pro forma valuation of roughly $4.35 billion. Shares fell over 10% on day one. Vacasa rode record post-pandemic travel demand into 2021, reporting $889 million in revenue, but the tailwind didn’t last. As travel demand normalized and rental supply increased industry-wide, Vacasa faced rising “homeowner churn,” with owners leaving faster than new ones joined.

Market Moves Since IPO

The numbers tell the story plainly. Vacasa’s home count fell from roughly 43,000 in early 2023 to 42,000 by year-end, then slid another 12% through 2024. Full-year 2024 revenue was $910.5 million, down 19% from $1.12 billion in 2023, with a net loss of $154.9 million. Vacasa also took a $244 million impairment charge, cut its workforce by roughly 13%, and cycled through three CEOs in five years. Altogether, the stock lost 97% of its value in its first three years, and nearly all of it by the time it was taken private. (SEC.gov)

By late 2024, Vacasa’s board began exploring a sale, agreeing on December 30 to be acquired by rival property manager Casago, taking it private again. After a brief competing bid from Davidson Kempner, shareholders approved $5.30 per share, and the deal closed April 30, 2025, for roughly $47.4 million, ending Vacasa’s run as a public company. It now operates as “A Casago Company,” with its board and top executives having resigned.

z

Nearly all of Vacasa’s value creation happened before it ever rang the Nasdaq bell. Its valuation grew roughly 4.35x, from just over $1 billion at its 2019 unicorn round to $4.35 billion at its SPAC debut two years later, gains captured entirely by private investors. Public shareholders who bought at the listing watched the stock lose 97% of its value over the next three years. An IPO is a liquidity event, not a guarantee of success, and Vacasa shows why: the growth had already happened, and the risk landed on public markets instead. That’s exactly the pattern that makes the Prime Unicorn Index so valuable, giving investors a way to track a company’s performance while it’s still private, rather than learning the hard way once it’s too late.

Vacasa’s collapse also illustrates the same risk from the other direction: sometimes the signs that a valuation has run ahead of the fundamentals are visible well before the correction actually happens, but investors have had no real way to act on that view in the private markets the way they can in public ones. The Prime Unicorn Index gives qualified investors exactly that tool, offering the ability to take short positions on private company shares, not just long ones. A private company riding hype into a valuation the market ultimately can’t support, the way Vacasa did heading into its SPAC debut, is exactly the kind of scenario where shorting lets sophisticated investors express that skepticism and manage risk before the public markets ever get the chance to correct it themselves.

Vacasa’s arc, from a bootstrapped side project to the industry’s first unicorn, to a multibillion-dollar public listing, and back into private hands at a fraction of its peak value, is a reminder of how quickly fortunes shift in the private markets. As you plan this summer’s getaway, remember that some of the biggest names behind those listings have been on a wild ride of their own to get there.